Credit Score Optimization for 2026: Boost Your Score by 50 Points in 6 Months

In the dynamic landscape of personal finance, a strong credit score is more than just a number; it’s a powerful tool that unlocks opportunities, saves you money, and provides peace of mind. As we look towards 2026, the importance of a robust credit profile continues to grow. Whether you’re planning to buy a home, secure a new car loan, or simply want access to better interest rates, understanding and implementing effective credit score optimization strategies is paramount. This comprehensive guide will walk you through four key strategies designed to boost your credit score by at least 50 points within a six-month timeframe, setting you up for financial success in the coming years.

Many people view their credit score as an unchangeable entity, a reflection of past financial decisions that are now set in stone. However, this couldn’t be further from the truth. Your credit score is a living, breathing metric that responds to your financial behavior. With consistent effort and the right approach, significant improvements are not only possible but entirely achievable. Our focus today is on actionable steps that yield tangible results, helping you navigate the complexities of credit reporting and come out stronger.

Before diving into the strategies, let’s briefly touch upon what exactly constitutes a credit score and why credit score optimization is so crucial. A credit score, typically FICO or VantageScore, is a three-digit number that lenders use to assess your creditworthiness. It’s a snapshot of your financial reliability, influenced by several factors. A higher score signifies lower risk to lenders, translating into more favorable loan terms, lower interest rates, and easier access to credit. Conversely, a lower score can lead to higher interest rates, stricter loan requirements, or even outright loan denials. Therefore, proactively managing and improving your credit score is a fundamental aspect of sound financial planning.

The journey to boosting your credit score by 50 points in six months requires dedication and a strategic mindset. It’s not about quick fixes but about establishing healthy financial habits that will serve you well in the long run. Let’s explore the four powerful strategies that will guide you on this path to enhanced financial health.

Strategy 1: Master Your Credit Utilization Ratio

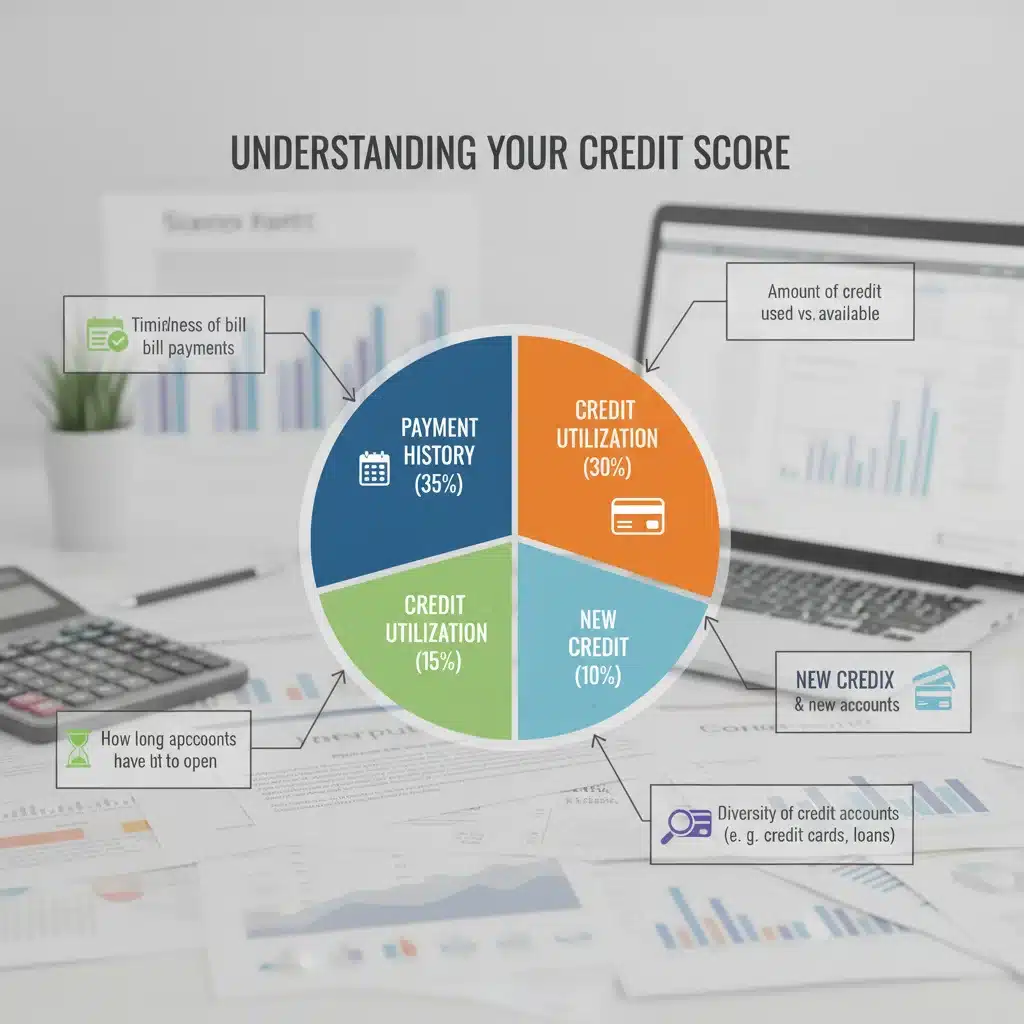

One of the most significant factors influencing your credit score, accounting for about 30% of your FICO score, is your credit utilization ratio. This ratio represents the amount of credit you’re currently using compared to the total amount of credit available to you. For example, if you have a credit card with a $10,000 limit and you’ve charged $3,000, your utilization ratio is 30% ($3,000 / $10,000). For optimal credit score optimization, experts generally recommend keeping this ratio below 30% across all your credit accounts, and ideally even lower, closer to 10% for the best scores.

Understanding the Impact of Credit Utilization

A high credit utilization ratio signals to lenders that you might be over-reliant on credit and potentially at risk of default. Even if you pay your bills on time, a high utilization can drag down your score. Conversely, a low utilization ratio demonstrates responsible credit management and indicates that you have plenty of available credit, which is seen favorably by credit bureaus.

Actionable Steps to Reduce Your Utilization Ratio:

- Pay Down Balances Strategically: Focus on paying down your credit card balances, especially those with the highest utilization. If you have multiple cards, prioritize the one with the highest balance relative to its limit. Even small, consistent payments above the minimum can make a big difference over six months.

- Make Multiple Payments Per Month: Instead of waiting for your statement due date, consider making payments throughout the month. Credit card companies often report your balance to credit bureaus based on your statement closing date. By making payments before this date, you can ensure a lower balance is reported, thus immediately reducing your utilization ratio. This is a highly effective, often overlooked, tactic for rapid credit score optimization.

- Increase Your Credit Limit (with Caution): If you have a good payment history and a stable income, you might consider requesting a credit limit increase on one of your existing cards. This increases your total available credit without adding new debt. However, only do this if you are confident you won’t be tempted to spend more. An increased limit only helps if your spending remains the same or decreases relative to the new limit.

- Avoid Closing Old Accounts: While it might seem counterintuitive, closing old credit card accounts can actually hurt your utilization ratio. When you close an account, you reduce your total available credit, which can cause your utilization ratio to jump if you carry balances on other cards. Keep old accounts open, even if you don’t use them, as long as they don’t have annual fees that you can’t justify.

- Consolidate Debt (Carefully): For those with significant credit card debt, a debt consolidation loan with a lower interest rate can be an option. This moves high-interest credit card debt into a single installment loan. While it doesn’t reduce the total amount of debt, it can free up your credit card limits, thereby lowering your utilization ratio on revolving accounts. Be cautious and ensure the new loan’s terms are favorable.

By diligently applying these steps, you can significantly improve your credit utilization ratio, which will have a profound positive effect on your credit score within the six-month target period for your credit score optimization goals.

Strategy 2: Ensure Timely Payments – The Foundation of Good Credit

Payment history is the most critical factor in your credit score, accounting for a massive 35% of your FICO score. This means that even a single late payment can have a devastating impact on your score, potentially dropping it by dozens of points. Conversely, a consistent history of on-time payments is the bedrock of excellent credit and is absolutely essential for any serious credit score optimization effort.

Why Payment History Matters Most

Lenders want to see evidence that you are responsible and reliable. Your payment history is the clearest indicator of your ability and willingness to repay borrowed money. Every on-time payment reinforces your creditworthiness, while every late payment (typically 30 days or more past due) signals risk.

Practical Steps for Flawless Payment History:

- Set Up Automatic Payments: This is arguably the simplest yet most effective way to ensure you never miss a payment. Most banks and credit card companies offer automatic payment options. You can set them up to pay the minimum amount due or the full balance each month. This eliminates the risk of forgetting a payment date.

- Use Payment Reminders: If automatic payments aren’t an option or you prefer manual control, utilize digital calendars, smartphone apps, or email reminders to alert you a few days before each payment is due. This gives you ample time to make the payment.

- Create a Payment Calendar: Physically write down all your due dates on a calendar you check regularly. Seeing your financial obligations laid out can help you stay organized and proactive.

- Align Due Dates: Contact your creditors and inquire about changing your payment due dates. If you can align most of your bills to fall around your payday, it can simplify your budgeting and reduce the chance of missing payments.

- Pay More Than the Minimum: While paying on time is crucial, paying more than the minimum due, especially on credit cards, is highly beneficial. It reduces your overall interest paid and helps lower your credit utilization ratio faster, contributing to overall credit score optimization.

- What to Do if You Miss a Payment (Act Fast!): If you realize you’ve missed a payment, act immediately. If you pay within a few days or weeks of the due date, it might not be reported to the credit bureaus as late (which typically happens after 30 days). Contact your creditor, explain the situation, and make the payment as soon as possible. They might even waive a late fee if it’s your first time.

By making timely payments a non-negotiable habit, you establish a strong foundation for your credit score, allowing the other strategies to build upon it effectively. This consistent behavior over six months will undoubtedly contribute significantly to your 50-point credit score increase.

Strategy 3: Monitor Your Credit Report for Errors and Fraud

Even with perfect financial habits, your credit score optimization efforts can be undermined by inaccuracies or fraudulent activity on your credit report. Errors are surprisingly common, and they can range from incorrect personal information to accounts that don’t belong to you, or even duplicate entries. These errors can artificially lower your score, making it crucial to regularly monitor your credit reports.

Why Regular Monitoring is Non-Negotiable

The Fair Credit Reporting Act (FCRA) entitles you to a free copy of your credit report from each of the three major credit bureaus (Experian, Equifax, and TransUnion) once every 12 months. You can access these reports at AnnualCreditReport.com. Regularly reviewing these reports allows you to:

- Identify and dispute errors: Incorrect information can negatively impact your score.

- Detect identity theft: Fraudulent accounts opened in your name can severely damage your credit.

- Understand your credit profile: Seeing the data lenders use helps you make informed financial decisions.

Steps for Effective Credit Report Monitoring and Error Resolution:

- Stagger Your Report Requests: Instead of pulling all three reports at once, consider requesting one report every four months. For example, Experian in January, Equifax in May, and TransUnion in September. This allows you to monitor your credit throughout the year without paying for additional reports.

- Review Each Report Meticulously: When you receive your report, don’t just skim it. Check for:

- Personal Information: Ensure your name, address, and Social Security number are correct.

- Account Information: Verify all listed accounts are yours, including credit cards, loans, and mortgages. Check account numbers, credit limits, balances, and payment status for accuracy.

- Inquiries: Look for hard inquiries that you don’t recognize. Too many hard inquiries can lower your score.

- Public Records: Check for bankruptcies, judgments, or liens that may be incorrect or outdated.

- Dispute Errors Promptly: If you find an error, dispute it immediately with both the credit bureau and the creditor that reported the information. The FCRA requires credit bureaus to investigate disputes within 30 days (or 45 days in some cases).

- Gather Documentation: Collect any evidence that supports your claim (e.g., payment receipts, account statements).

- Write a Dispute Letter: Clearly state the error, why it’s incorrect, and include copies of your supporting documents. Send it via certified mail with a return receipt requested.

- Follow Up: Keep records of all correspondence and follow up if you don’t hear back within the stipulated timeframe.

- Consider Credit Monitoring Services: While not strictly necessary, some paid credit monitoring services can alert you to changes in your credit report in real-time, providing an extra layer of protection against fraud and errors. Many credit card companies also offer free credit score monitoring tools that can be very helpful for continuous credit score optimization.

Cleaning up errors on your credit report can provide an immediate boost to your score, sometimes significantly. It’s a proactive step that protects your financial identity and ensures your credit score accurately reflects your financial responsibility. Over six months, diligent monitoring and correction can contribute substantially to your 50-point goal.

Strategy 4: Diversify Your Credit Mix and Build Credit History

The length of your credit history (15% of your FICO score) and your credit mix (10% of your FICO score) are two other important factors in credit score optimization. While you can’t instantly make your credit history longer, you can take steps to diversify your credit accounts and establish new positive credit entries that will mature over time.

Understanding Credit Mix and Length of History

Credit mix refers to the different types of credit accounts you have, such as revolving credit (credit cards) and installment credit (mortgages, car loans, student loans). Lenders like to see that you can responsibly manage various types of credit. The length of your credit history is simply how long your oldest and newest accounts have been open, and the average age of all your accounts. A longer history generally indicates more experience managing credit.

Tactics to Improve Credit Mix and History:

- Become an Authorized User (Carefully): If you have a trusted family member or friend with excellent credit and a long, positive payment history on a credit card, they might add you as an authorized user. This can add their positive history to your credit report, potentially boosting your score. However, ensure they are responsible, as their negative actions could also impact you. Discuss this thoroughly beforehand.

- Consider a Secured Credit Card: If you have limited credit history or a poor score, a secured credit card is an excellent way to build or rebuild credit. You put down a deposit, which becomes your credit limit. This card works like a regular credit card, and your responsible usage (low utilization, on-time payments) is reported to the credit bureaus. After 6-12 months of good use, you can often graduate to an unsecured card and get your deposit back.

- Explore Credit-Builder Loans: These specialized loans are designed to help you build credit. The loan amount is typically held in a savings account or CD while you make monthly payments. Once the loan is fully repaid, you receive the money. The on-time payments are reported to credit bureaus, establishing a positive payment history and diversifying your credit mix with an installment loan.

- Report Rent and Utility Payments: Traditionally, rent and utility payments haven’t been included in credit reports unless they go to collections. However, services now exist that allow you to report these on-time payments to credit bureaus. Check with your landlord or utility providers, or consider services like RentReporters or Experian Boost, which can add positive payment history to your report. This can be a quick win for credit score optimization.

- Avoid Opening Too Many New Accounts Too Quickly: While diversifying your credit mix is good, opening several new accounts in a short period can be detrimental. Each new application results in a hard inquiry, which can slightly lower your score. Also, new accounts lower the average age of your credit history. Be selective and strategic about opening new lines of credit.

- Maintain Old Accounts: As mentioned in Strategy 1, keep your oldest accounts open and in good standing. These accounts contribute significantly to the length of your credit history, which is a positive factor.

By strategically adding new, responsibly managed accounts and ensuring your positive payment history is reported, you can enhance both your credit mix and the length of your credit history, moving you closer to your 50-point score increase in six months.

Putting It All Together: Your 6-Month Credit Score Optimization Plan

Achieving a 50-point increase in your credit score within six months is an ambitious but entirely attainable goal with consistent effort and adherence to these strategies. Here’s a summary of how to integrate these actions into a cohesive plan:

Month 1-2: Foundation and Assessment

- Get Your Credit Reports: Pull one free report (e.g., Experian) from AnnualCreditReport.com. Review it thoroughly for errors.

- Calculate Your Utilization: Add up all your credit card balances and compare them to your total credit limits. Identify cards with high utilization.

- Set Up Auto-Payments: Enroll all credit accounts in automatic payments for at least the minimum amount.

- Prioritize Debt Repayment: Focus on making extra payments on the credit card with the highest utilization.

- Begin Dispute Process: If you found errors, initiate disputes with the credit bureaus and creditors.

Month 3-4: Momentum and Diversification

- Pull Second Report: Get your next free report (e.g., Equifax) and review it. Follow up on previous disputes.

- Continue Reducing Utilization: Maintain aggressive payments on high-balance cards. Consider making multiple payments per month.

- Explore New Credit (If Needed): If your credit mix is poor or history is thin, research secured credit cards or credit-builder loans. Apply for one if it aligns with your goals and you’re confident in managing it responsibly.

- Consider Authorized User Option: Discuss with a trusted individual if becoming an authorized user is a viable option for you.

Month 5-6: Refinement and Long-Term Habits

- Pull Third Report: Access your final free report (e.g., TransUnion). Verify all disputes are resolved and check for any new discrepancies.

- Maintain Low Utilization: Aim to keep all credit card utilization below 10-20%.

- Solidify Payment Habits: Ensure all payments are consistently on time. Consider paying your full credit card balances every month if possible.

- Review Progress: Compare your current credit score (many credit card apps offer free scores) to where you started. You should see significant improvement.

- Plan for the Future: Think about your financial goals for 2026 and beyond. How will your improved credit score help you achieve them?

The Long-Term Benefits of Credit Score Optimization

While the immediate goal is a 50-point boost in six months, the true value of credit score optimization lies in the long-term benefits it provides. A consistently high credit score can save you thousands of dollars over your lifetime through lower interest rates on mortgages, car loans, and personal loans. It can also make it easier to rent an apartment, get better insurance rates, and even secure certain jobs.

Remember, building and maintaining excellent credit is an ongoing process. The habits you establish during this six-month challenge – diligent payment, careful utilization, proactive monitoring, and strategic credit building – will serve as the foundation for a lifetime of financial well-being. Embrace these strategies, stay disciplined, and watch your financial future flourish as you head into 2026 with a powerful, optimized credit score.

Don’t underestimate the power of small, consistent actions. Each on-time payment, each reduction in your credit card balance, and each error corrected on your report contributes to the larger goal. By focusing on these four core strategies, you are not just improving a number; you are investing in your financial freedom and unlocking a world of opportunities. Start your credit score optimization journey today and prepare for a more secure and prosperous 2026.