Roth vs. Traditional IRA 2026: Tax Savings Explained

Comparing Roth vs. Traditional IRAs in 2026: Which Option Saves You More on Taxes?

Navigating the complex world of retirement savings can feel like deciphering a cryptic code, especially when faced with choices like the Roth Traditional IRA. As we look ahead to 2026, understanding the nuances between these two powerful retirement vehicles is more critical than ever. The decisions you make today about your IRA contributions can significantly impact your tax burden in retirement, determining whether you pay taxes now or later.

For many, the question isn’t whether to save for retirement, but how. The Roth IRA and the Traditional IRA both offer enticing benefits, yet they operate on fundamentally different tax principles. One provides immediate tax relief, while the other promises tax-free income in your golden years. Which one is right for you? This comprehensive guide will delve deep into the mechanics of both, explore the latest considerations for 2026, and help you determine which option aligns best with your financial goals and tax outlook.

Understanding the distinction between a Roth Traditional IRA is not merely an academic exercise; it’s a strategic move that could save you thousands, if not tens of thousands, of dollars over your lifetime. We’ll break down contribution rules, income limitations, withdrawal policies, and other critical factors that influence your choice. Prepare to gain clarity and confidence in your retirement planning decisions.

The Core Difference: Tax Treatment Explained

The most fundamental difference between a Roth IRA and a Traditional IRA lies in their tax treatment. This distinction is paramount and dictates much of the strategic thinking behind choosing one over the other.

Traditional IRA: Tax Deduction Now, Taxes Later

A Traditional IRA allows you to contribute pre-tax dollars, meaning your contributions may be tax-deductible in the year they are made. This can lead to an immediate reduction in your taxable income, potentially lowering your current tax bill. For instance, if you contribute $6,500 to a Traditional IRA in 2026 (assuming contribution limits are similar to previous years, adjusted for inflation), and you’re in the 22% tax bracket, you could save $1,430 on your taxes that year. The money in your Traditional IRA then grows tax-deferred. You don’t pay taxes on the investment gains until you withdraw the money in retirement. At that point, both your original contributions (if deducted) and all earnings are taxed as ordinary income.

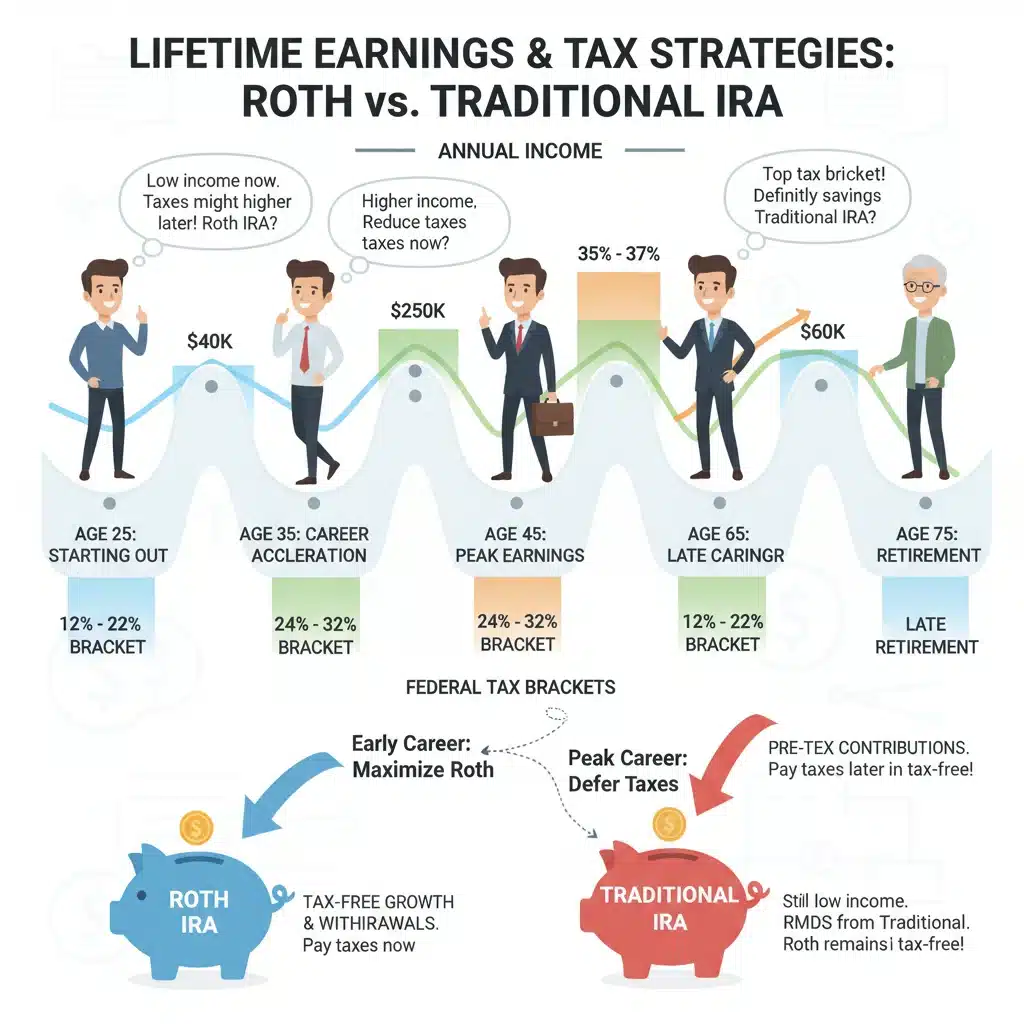

This structure is particularly appealing to individuals who expect to be in a higher tax bracket during their working years than they will be in retirement. By taking a tax deduction now, they effectively defer paying taxes until a time when their income (and likely their tax rate) is lower. This strategy maximizes the immediate tax benefit.

Roth IRA: Taxes Now, Tax-Free Later

Conversely, a Roth IRA operates on an opposite tax principle. Contributions to a Roth IRA are made with after-tax dollars, meaning you do not get an upfront tax deduction for your contributions. However, the significant advantage of a Roth IRA is that all qualified withdrawals in retirement are completely tax-free. This includes both your original contributions and all the investment earnings your account has generated over decades. This tax-free growth and withdrawal feature is a major draw for many investors.

The Roth IRA is often favored by individuals who anticipate being in a higher tax bracket during retirement than they are currently. By paying taxes on their contributions now, they lock in their current (presumably lower) tax rate and avoid paying taxes on what could be substantial investment gains in the future. This can be an incredibly powerful tool for long-term wealth accumulation, especially for younger investors with many years of growth ahead.

When considering the Roth Traditional IRA debate, understanding these core tax treatments is your first step. It frames the entire discussion around when you prefer to pay your taxes: now or later.

Contribution Limits and Income Restrictions for 2026

Both Roth and Traditional IRAs come with specific rules regarding how much you can contribute each year and who is eligible to contribute. While exact figures for 2026 are subject to IRS adjustments, we can base our discussion on current trends and anticipated changes.

IRA Contribution Limits

Historically, the IRS adjusts IRA contribution limits annually for inflation. For 2025, the total contribution limit for IRAs (both Roth and Traditional combined) is expected to be around $7,000, with an additional catch-up contribution of $1,000 for those aged 50 and over. While 2026 figures are not yet released, it’s reasonable to expect a similar or slightly higher limit. This means that, regardless of whether you choose a Roth, Traditional, or a combination of both, the total amount you can contribute across all your IRAs in a given year will be capped.

It’s crucial to stay updated on these limits as they directly impact your savings potential. Maxing out your IRA contributions each year is a cornerstone of effective retirement planning, helping you leverage the tax advantages offered by either a Roth Traditional IRA.

Income Limitations for Roth IRAs

One significant factor that differentiates the Roth IRA from the Traditional IRA is the income limitation for direct contributions. For 2026, it’s highly probable that there will continue to be modified adjusted gross income (MAGI) phase-out ranges for contributing directly to a Roth IRA. If your MAGI exceeds these limits, your ability to contribute directly to a Roth IRA will be reduced or eliminated.

For example, for single filers in 2025, the MAGI phase-out range for Roth IRA contributions was roughly between $146,000 and $161,000. For married couples filing jointly, it was between $230,000 and $240,000. If your income falls within these ranges, your maximum Roth contribution is gradually reduced. If your income exceeds the upper limit, you cannot contribute directly to a Roth IRA.

If you find yourself above the Roth IRA income limits, you might still have options, such as the "backdoor Roth IRA" strategy. This involves contributing to a non-deductible Traditional IRA and then converting it to a Roth IRA. While this strategy can be complex and has specific rules (especially regarding the pro-rata rule if you have other pre-tax IRA accounts), it allows high-income earners to still benefit from the tax-free growth of a Roth IRA. Consulting a financial advisor is highly recommended if you’re considering this approach.

Income Limitations for Traditional IRAs

Traditional IRAs do not have income limitations for contributions. Anyone with earned income can contribute to a Traditional IRA. However, the ability to deduct those contributions on your taxes does depend on your income and whether you or your spouse are covered by a retirement plan at work (like a 401(k) or 403(b)).

If neither you nor your spouse is covered by a workplace retirement plan, your Traditional IRA contributions are fully tax-deductible, regardless of your income. If you are covered by a workplace plan, the deductibility of your Traditional IRA contributions phases out at higher income levels. For 2026, these income thresholds will likely be updated, but the principle remains the same: higher earners covered by a workplace plan may not be able to deduct their Traditional IRA contributions.

If your Traditional IRA contributions are not deductible, the earnings still grow tax-deferred, but your original contributions will not be taxed upon withdrawal. This scenario is often where the "backdoor Roth" strategy becomes relevant, as converting non-deductible Traditional IRA contributions to a Roth allows for tax-free growth and withdrawals.

Withdrawal Rules and Flexibility

Understanding when and how you can access your money is another critical aspect of the Roth Traditional IRA comparison.

Traditional IRA Withdrawals

With a Traditional IRA, withdrawals in retirement generally begin at age 59½. Any withdrawals before this age are typically subject to a 10% early withdrawal penalty, in addition to being taxed as ordinary income. There are a few exceptions to the early withdrawal penalty, such as for unreimbursed medical expenses, higher education expenses, or a first-time home purchase (up to $10,000). Once you reach age 73 (as per current Secure Act 2.0 provisions, subject to change), you must begin taking Required Minimum Distributions (RMDs) from your Traditional IRA, whether you need the money or not. Failure to take RMDs can result in a significant penalty.

Roth IRA Withdrawals: The Power of Tax-Free Income

Roth IRAs offer much more flexibility when it comes to withdrawals. Since your contributions were already taxed, you can withdraw your original contributions at any time, for any reason, tax-free and penalty-free. This provides an excellent emergency fund or a flexible source of funds for major life events, without dipping into your tax-deferred growth.

For earnings to be withdrawn tax-free and penalty-free, two conditions must be met: you must be at least 59½ years old, AND five years must have passed since your first Roth IRA contribution (the "five-year rule"). If these conditions are met, all withdrawals, including earnings, are completely tax-free. If you withdraw earnings before meeting these conditions, they may be subject to income tax and a 10% early withdrawal penalty, though there are exceptions similar to Traditional IRAs.

Unlike Traditional IRAs, Roth IRAs do not have RMDs for the original owner. This means you can leave the money in your Roth IRA to continue growing tax-free for as long as you live, and then pass it on to your heirs, who will also receive tax-free distributions (though specific rules apply to beneficiaries). This RMD-free feature makes the Roth IRA an excellent estate planning tool.

When to Choose a Traditional IRA: Ideal Scenarios for 2026

The Traditional IRA shines in specific financial situations, particularly for those who can benefit from upfront tax deductions.

Higher Current Tax Bracket

If you are currently in a relatively high tax bracket and anticipate being in a lower tax bracket during retirement, a Traditional IRA is likely your better choice. The immediate tax deduction reduces your current taxable income, saving you money on taxes today. For example, a mid-career professional earning a substantial salary will likely benefit more from the upfront deduction than someone just starting their career with lower income.

Need for Immediate Tax Savings

For individuals and families who are looking to minimize their current tax liability, the Traditional IRA provides a direct mechanism to do so. The tax deduction can reduce your overall tax bill, freeing up funds for other financial goals or simply enhancing your current cash flow. This can be especially important for those managing significant expenses, such as a mortgage or childcare costs.

Above Roth IRA Income Limits (Without Backdoor Strategy)

If your income exceeds the limits for direct Roth IRA contributions and you are either unwilling or unable to utilize the backdoor Roth strategy, a Traditional IRA remains a viable option for tax-advantaged retirement savings. While your contributions might not be deductible if you’re covered by a workplace plan and earn a high income, the tax-deferred growth is still a valuable benefit compared to a taxable brokerage account.

No Need for Tax-Free Withdrawals

Some individuals may have other sources of tax-free income in retirement (e.g., substantial municipal bond interest) or may simply prefer to pay taxes later. If the prospect of tax-free withdrawals isn’t a primary driver for your retirement planning, the Traditional IRA’s deferred tax model might be more appealing.

Ultimately, the choice for a Roth Traditional IRA depends on your current financial picture, your tax bracket today, and your expectations for your tax bracket in retirement.

When to Choose a Roth IRA: Ideal Scenarios for 2026

The Roth IRA is a powerful tool for specific investor profiles, particularly those focused on future tax savings and flexibility.

Lower Current Tax Bracket

If you are currently in a lower tax bracket than you expect to be in during retirement, a Roth IRA is often the optimal choice. By paying taxes on your contributions now, you lock in your current (lower) tax rate. This strategy is incredibly beneficial for young professionals, students, or those in transitional career phases where their income is relatively low but is expected to grow significantly over time. The tax-free growth and withdrawals in retirement can lead to substantial savings.

Anticipated Higher Future Tax Bracket

Many financial experts predict that tax rates may rise in the future due to government spending and demographic shifts. If you believe you will be in a higher tax bracket in retirement than you are today, contributing to a Roth IRA allows you to pay taxes at today’s potentially lower rates, ensuring all your qualified withdrawals in retirement are tax-free. This acts as a hedge against future tax increases.

Desire for Tax-Free Income in Retirement

The allure of tax-free income in retirement is a major draw for the Roth IRA. Knowing that a portion of your retirement income will be completely free from federal (and often state) income taxes provides immense peace of mind and simplifies retirement budgeting. This is especially valuable for those who want to minimize their taxable income in retirement to potentially avoid higher Medicare premiums or taxation of Social Security benefits.

Flexibility with Withdrawals

The ability to withdraw your original contributions from a Roth IRA tax-free and penalty-free at any time offers unparalleled flexibility. This can serve as an emergency fund or a source of funds for significant life events, without disrupting your long-term investment growth. For younger investors who might need access to funds before retirement, this feature can be very attractive.

No Required Minimum Distributions (RMDs) for Original Owner

The absence of RMDs for the original owner of a Roth IRA is a significant advantage, particularly for those who wish to leave a larger legacy to their heirs. The money can continue to grow tax-free for their entire lifetime, and then be passed on to beneficiaries who also benefit from tax-free distributions (though specific rules apply to beneficiaries). This makes the Roth IRA an excellent estate planning tool.

When weighing the Roth Traditional IRA options, consider your long-term tax outlook, your need for current tax deductions, and your desire for withdrawal flexibility.

The Backdoor Roth IRA: A Strategy for High Earners in 2026

For high-income earners who exceed the direct Roth IRA contribution limits, the "backdoor Roth IRA" strategy remains a popular and legitimate method to get money into a Roth account. This strategy involves two main steps:

- Contribute to a Non-Deductible Traditional IRA: First, you contribute to a Traditional IRA. If your income is above the IRS thresholds for deducting Traditional IRA contributions (and you are covered by a workplace plan), these contributions will be non-deductible. This means you don’t get an upfront tax break, but the money still grows tax-deferred.

- Convert the Traditional IRA to a Roth IRA: Shortly after contributing, you convert the non-deductible Traditional IRA balance to a Roth IRA. Since your initial contribution was non-deductible (and thus already taxed), this conversion is generally tax-free. Any earnings that accrued between the contribution and conversion would be taxable upon conversion, but if done quickly, this amount is usually minimal.

The key challenge with the backdoor Roth strategy is the "pro-rata rule." This rule states that if you have any other pre-tax Traditional IRA, SEP IRA, or SIMPLE IRA accounts, a portion of your conversion will be taxable. The IRS looks at all your Traditional IRA balances (both deductible and non-deductible) when determining the taxable portion of a Roth conversion. To avoid this, it’s often advisable to have no other pre-tax IRA balances, or to roll them into a 401(k) if your plan allows, before executing a backdoor Roth.

While the backdoor Roth has faced scrutiny in the past from lawmakers, it has consistently remained a legal strategy. However, tax laws can change, so it’s always wise to consult with a tax professional to ensure you are following the latest regulations and that this strategy is appropriate for your specific situation in 2026.

Deciding Between Roth and Traditional IRA: Key Considerations for 2026

Making the choice between a Roth Traditional IRA isn’t a one-size-fits-all decision. It requires a careful evaluation of your personal financial situation, current and projected income, and long-term goals. Here are some key factors to consider:

1. Your Current vs. Future Tax Bracket

This is arguably the most important factor. If you believe your income (and thus your tax bracket) will be higher in retirement than it is now, a Roth IRA is generally preferable. You pay taxes at a lower rate today to enjoy tax-free withdrawals later. If you expect to be in a lower tax bracket in retirement, a Traditional IRA’s upfront deduction makes more sense, as you defer taxes until you’re in a lower bracket.

2. Income Levels and Eligibility

As discussed, direct Roth IRA contributions have income limits. If your income is above these limits, you’ll need to consider the backdoor Roth strategy or opt for a Traditional IRA. For Traditional IRAs, while there are no income limits for contributions, the deductibility of those contributions depends on your income and whether you’re covered by a workplace retirement plan.

3. Need for Immediate Tax Savings

If reducing your current taxable income is a priority, a Traditional IRA offers an immediate tax deduction that a Roth IRA does not. This can be beneficial for managing current expenses or qualifying for other tax credits and deductions that are tied to your adjusted gross income.

4. Desire for Tax-Free Income in Retirement

The appeal of tax-free withdrawals in retirement is a significant advantage of the Roth IRA. This can provide greater certainty in retirement planning, as you won’t have to worry about future tax rate changes impacting a portion of your income.

5. Flexibility and Access to Funds

Roth IRAs offer more flexibility, allowing you to withdraw contributions tax-free and penalty-free at any time. This can be a valuable feature for liquidity, although it’s generally best to avoid dipping into retirement savings unless absolutely necessary. Traditional IRAs have stricter rules and penalties for early withdrawals.

6. Estate Planning Goals

For those looking to leave a tax-efficient inheritance, the Roth IRA’s lack of RMDs for the original owner and tax-free distributions to beneficiaries (under certain rules) make it a superior estate planning tool compared to a Traditional IRA.

7. Age and Time Horizon

Younger investors with many years until retirement often benefit more from a Roth IRA due to the long runway for tax-free growth. The compounding effect on tax-free earnings over decades can be immense. Older investors closer to retirement might lean towards a Traditional IRA if their current tax bracket is higher and they anticipate a lower one soon.

Combining Roth and Traditional IRAs: A Hybrid Approach

It’s important to remember that you don’t necessarily have to choose one or the other. Many individuals benefit from a hybrid approach, contributing to both a Roth IRA and a Traditional IRA, or even utilizing a 401(k) alongside an IRA. This strategy, often referred to as "tax diversification," allows you to hedge against future tax uncertainty.

By having both pre-tax (Traditional) and after-tax (Roth) retirement accounts, you gain flexibility in retirement to draw from whichever account type offers the most tax advantage at that specific time. For example, in a year where your income is low in retirement, you might draw from your Traditional IRA to fill up lower tax brackets. In years where you need more income or anticipate a higher tax bill, you could draw from your Roth IRA tax-free.

This balanced approach helps mitigate the risk of guessing future tax rates correctly and provides more control over your taxable income in retirement. It’s a sophisticated strategy that can be highly effective for optimizing your long-term tax situation.

The Impact of Secure Act 2.0 and Future Legislation

The Secure Act 2.0, enacted in late 2022, brought significant changes to retirement planning, including adjustments to RMD ages and new provisions for Roth 401(k)s. While most of its provisions are already in effect, it highlights the dynamic nature of retirement tax laws. As we approach 2026, it’s crucial to stay informed about any potential new legislation that could further impact the Roth Traditional IRA landscape.

For instance, discussions around federal budget deficits and potential tax reforms could lead to changes in tax brackets, contribution limits, or even the rules governing Roth conversions. Staying abreast of these developments, perhaps through reputable financial news sources or a trusted financial advisor, is paramount for making informed decisions.

Common Misconceptions About Roth vs. Traditional IRAs

Despite their popularity, several misconceptions persist regarding Roth and Traditional IRAs. Clearing these up can help you make a more informed choice.

- "Roth is always better for young people." While often true due to the longer runway for tax-free growth, a young person in a very low current tax bracket might get more benefit from a Traditional IRA deduction if they need to reduce their current taxable income to qualify for certain credits or benefits. It’s about projected future tax rates versus current needs.

- "Traditional IRAs are only for high earners." Not true. Anyone with earned income can contribute. The key is whether you can deduct the contributions, which depends on income and workplace plan coverage. Even if non-deductible, the tax-deferred growth is still valuable.

- "You can only have one type of IRA." Absolutely false. You can contribute to both a Roth and a Traditional IRA in the same year, as long as your total contributions do not exceed the annual limit. This allows for excellent tax diversification.

- "Roth IRAs are only for investing in stocks." Both Roth and Traditional IRAs can hold a wide variety of investments, including stocks, bonds, mutual funds, ETFs, and even real estate (through specialized custodians). The account type dictates the tax treatment, not the investment options.

Seeking Professional Guidance for Your IRA Decisions

The decision between a Roth Traditional IRA, or a combination of both, is highly personal and depends on a multitude of factors unique to your financial situation. While this guide provides a comprehensive overview for 2026, it is not a substitute for personalized financial advice.

A qualified financial advisor can help you:

- Analyze your current income, expenses, and tax bracket.

- Project your likely income and tax bracket in retirement.

- Evaluate your eligibility for various IRA contributions and deductions.

- Determine if a backdoor Roth strategy is suitable and how to execute it properly.

- Integrate your IRA strategy with other retirement accounts (like 401(k)s) and overall financial planning.

- Stay updated on federal tax law changes that could impact your retirement savings.

Investing in professional financial guidance can provide clarity, optimize your tax strategy, and ultimately help you achieve a more secure and prosperous retirement. Don’t leave your retirement savings to chance; make informed decisions based on expert advice tailored to your needs.

Conclusion: Strategic Choices for Your 2026 Retirement Plan

The choice between a Roth IRA and a Traditional IRA for 2026 is a pivotal decision in your retirement planning journey. Both offer significant tax advantages, but they cater to different financial situations and future tax outlooks. The Traditional IRA provides immediate tax deductions and tax-deferred growth, ideal for those who anticipate a lower tax bracket in retirement. The Roth IRA, on the other hand, offers tax-free growth and withdrawals, making it an excellent choice for those who expect to be in a higher tax bracket in the future or desire tax-free income in retirement.

Consider your current income, your long-term income projections, your age, and your overall financial goals. Don’t overlook the power of tax diversification by utilizing both types of accounts, or the potential of the backdoor Roth for high-income earners. By carefully evaluating these factors and staying informed about potential legislative changes, you can strategically position your retirement savings to maximize your tax benefits and build a robust financial future. Make your Roth Traditional IRA decision for 2026 a well-informed one, setting the stage for a comfortable and tax-efficient retirement.

Contributions for 2026: Smart Money Moves")

in 2025: Boost Savings by $2,500 Annually")

in 2026: New $23,000 Limit Explained")