Social Security 2026 COLA: Understanding the 3.2% Increase

The financial landscape for retirees and other beneficiaries of Social Security is constantly evolving, with annual Cost-of-Living Adjustments (COLAs) playing a pivotal role in maintaining purchasing power. As we look ahead to 2026, projections suggest a significant 3.2% increase in the Social Security COLA, a figure that demands careful examination for anyone relying on these crucial benefits. This anticipated adjustment, while not yet official, offers a glimpse into the economic forces at play and how they might shape the financial well-being of millions of Americans. Understanding the intricacies of the Social Security COLA 2026 is paramount for effective financial planning and ensuring that your retirement income keeps pace with the cost of living.

What is the Social Security COLA and Why Does it Matter?

The Cost-of-Living Adjustment, or COLA, is an annual increase in Social Security and Supplemental Security Income (SSI) benefits. Its primary purpose is to help beneficiaries cope with inflation, ensuring that their purchasing power isn’t eroded over time. Without COLA, the fixed income of retirees would gradually lose value as the cost of goods and services rises, making it increasingly difficult to afford necessities. The Social Security Administration (SSA) announces the official COLA each October, based on the Consumer Price Index for Urban Wage Earners and Clerical Workers (CPI-W) from the third quarter of the current year compared to the third quarter of the previous year.

For millions of Americans, Social Security benefits represent a significant, often primary, source of income in retirement, or due to disability or survivor status. Therefore, the annual COLA is not just a statistical adjustment; it’s a vital lifeline that directly impacts the quality of life for a substantial portion of the population. A higher COLA means more money in beneficiaries’ pockets, which can help cover rising expenses for housing, food, healthcare, and transportation. Conversely, a low or non-existent COLA can strain household budgets, forcing difficult choices and potentially leading to financial hardship. The projected Social Security COLA 2026 of 3.2% signals a continued effort to mitigate the effects of inflation on these essential benefits.

Decoding the 3.2% Social Security COLA for 2026

The projected 3.2% Social Security COLA 2026 is based on economic forecasts and current inflationary trends. While this number is not final and is subject to change based on actual CPI-W data later in the year, it provides a strong indication of what beneficiaries can expect. This percentage is derived from an analysis of various economic indicators, particularly inflation rates. When the cost of living increases, as measured by the CPI-W, Social Security benefits are adjusted upwards to maintain their real value. A 3.2% increase, if it materializes, would mean that for every $1,000 in monthly Social Security benefits, beneficiaries would receive an additional $32. This seemingly small increment can accumulate significantly over a year, providing crucial support for daily expenses.

Understanding how this projection is calculated involves looking at the broader economic picture. Factors such as energy prices, food costs, housing inflation, and healthcare expenditures all contribute to the CPI-W. When these components rise, the overall index increases, triggering a COLA. The 3.2% projection suggests that economists anticipate a continued, albeit potentially moderating, inflationary environment leading up to the third quarter of 2025 (the period used for the 2026 COLA calculation). It’s a forward-looking estimate that aims to give beneficiaries and policymakers an early understanding of potential adjustments, allowing for better financial planning and policy discussions. The accuracy of these projections is critical, as they set expectations for millions of households.

Historical Context: How Does 3.2% Compare to Previous COLAs?

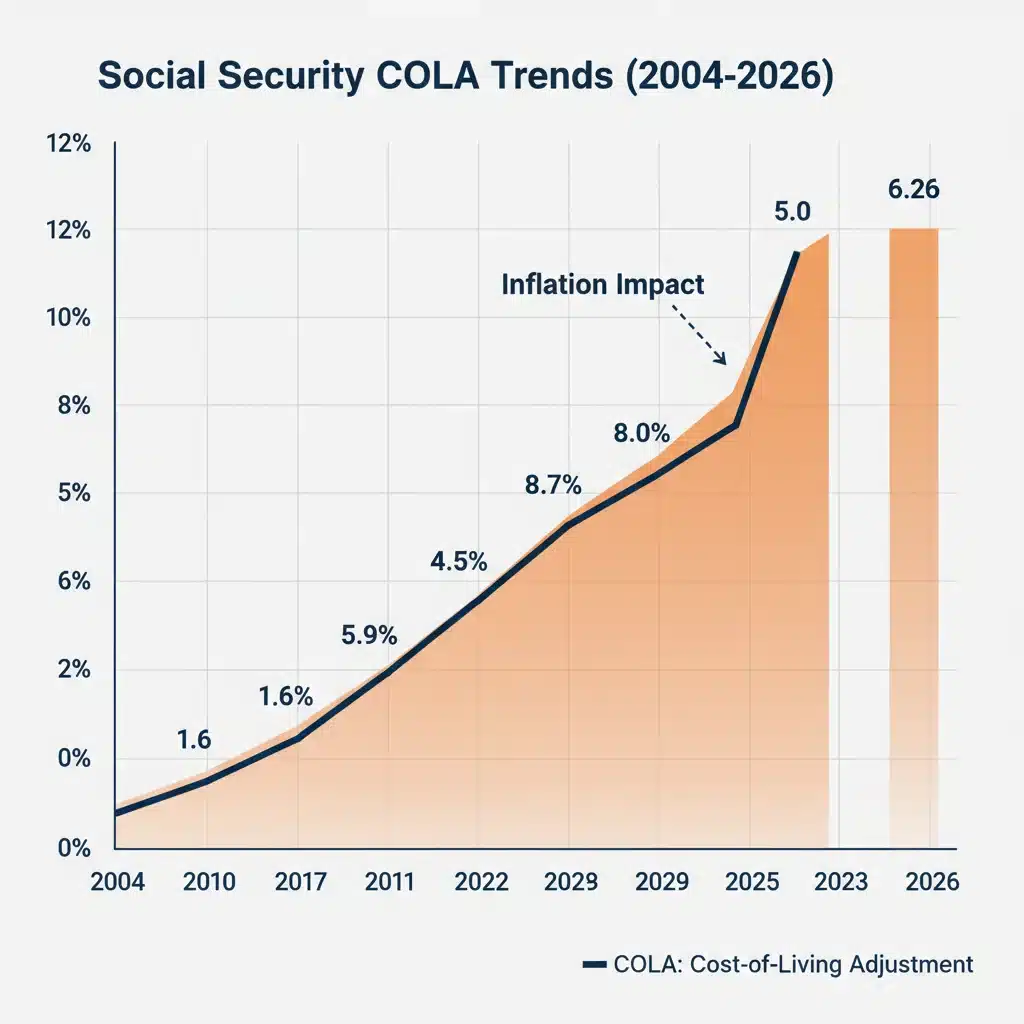

To fully appreciate the significance of a projected 3.2% Social Security COLA 2026, it’s helpful to place it within a historical context. Recent years have seen some of the largest COLAs in decades, driven by unprecedented inflation. For instance, the 2022 COLA was 5.9%, and the 2023 COLA reached a substantial 8.7%, the highest since 1981. These significant increases were a direct response to the surge in inflation observed during and after the COVID-19 pandemic, which impacted everything from consumer goods to energy prices.

Prior to these recent spikes, COLAs were generally more modest, often hovering around 1% to 3% for many years. There were even a few years with no COLA at all when inflation was negligible or negative. A 3.2% COLA, while lower than the recent highs, would still be considered a healthy adjustment when viewed against the longer-term historical average. It suggests a return to a more typical, yet still impactful, level of inflation adjustment. This historical perspective is vital because it helps beneficiaries understand that while the larger COLAs of recent years were exceptional, a 3.2% adjustment for the Social Security COLA 2026 is a meaningful step in preserving their financial stability. It reflects a continued recognition of the need to protect seniors and other beneficiaries from the eroding effects of rising costs.

The Economic Factors Driving the 2026 COLA Projection

Several key economic factors influence the projection of the 3.2% Social Security COLA 2026. At the forefront is inflation, specifically as measured by the CPI-W. This index tracks changes in the prices of a basket of consumer goods and services, including food, housing, transportation, medical care, and clothing. Persistent inflation, even if it moderates from recent peaks, will continue to push the CPI-W upwards, thus necessitating a COLA.

Beyond the direct CPI-W calculation, broader economic conditions play a crucial role. These include:

- Energy Prices: Fluctuations in global oil and gas markets directly impact transportation costs and utility bills, which are significant components of the CPI-W. Geopolitical events and supply chain issues can cause volatility in these prices, influencing COLA projections.

- Food Costs: Agricultural yields, global demand, and supply chain efficiencies all affect food prices. Increases in this sector disproportionately impact lower-income households and retirees, making it a critical factor for COLA.

- Housing Market: Rent and homeownership costs, including mortgage interest and property taxes, are substantial expenses. A robust or inflationary housing market can significantly contribute to overall inflation and thus to the COLA.

- Labor Market: Wage growth, while not directly part of the CPI-W calculation, can indicate underlying inflationary pressures. Strong wage growth can lead to increased consumer spending, which in turn can push up prices.

- Federal Reserve Policy: The Federal Reserve’s monetary policy, particularly interest rate decisions, aims to control inflation. The effectiveness of these policies in cooling the economy without triggering a recession will indirectly influence future COLA figures.

The 3.2% projection for the Social Security COLA 2026 reflects an expectation of continued, albeit possibly more stable, inflationary pressures compared to the volatile periods of 2021-2023. Economists are constantly monitoring these indicators to refine their forecasts, making the COLA a dynamic and often anticipated announcement each year.

Impact on Beneficiaries: Who Benefits Most from a 3.2% COLA?

A 3.2% Social Security COLA 2026 would provide a meaningful boost to the income of all Social Security beneficiaries. This includes retired workers, disabled workers, and survivors (spouses and children of deceased workers). While the percentage increase is uniform, the actual dollar amount will vary based on an individual’s current benefit amount. Those with higher monthly benefits will see a larger dollar increase, but the proportional increase in purchasing power is the same for everyone.

However, certain groups may feel the impact of a COLA more acutely:

- Low-Income Beneficiaries: For those whose Social Security benefits constitute a larger portion of their overall income, any increase, even a modest one, is critically important. It can mean the difference between affording essential goods and services or having to cut back.

- Beneficiaries with High Healthcare Costs: Healthcare expenses often rise faster than general inflation. While COLA helps, it may not always fully offset the rapid increase in medical premiums, prescription costs, and co-pays. However, a 3.2% increase still provides some buffer against these rising costs.

- Fixed-Income Retirees: Individuals who rely almost exclusively on Social Security and other fixed income sources are particularly vulnerable to inflation. The COLA is their primary mechanism for maintaining financial stability.

It’s also important to consider the potential interaction of COLA with other aspects of beneficiaries’ finances, such as Medicare premiums. Historically, Medicare Part B premiums have sometimes increased, absorbing a portion of the COLA. However, legislation like the ‘hold harmless’ provision often prevents Part B premiums from reducing a beneficiary’s net Social Security payment for most individuals. The net effect of the Social Security COLA 2026 on an individual’s take-home pay will depend on these various factors, but generally, it’s designed to be a positive adjustment.

Planning for the Future: Incorporating the COLA into Your Retirement Strategy

For current retirees and those nearing retirement, understanding the projected Social Security COLA 2026 is a critical component of effective financial planning. While 3.2% is a projection, it provides a valuable benchmark for adjusting your budget and future financial expectations. Here’s how you can incorporate this information:

- Review Your Budget: Use the projected COLA to estimate your increased Social Security income for 2026. Compare this to your anticipated expenses, especially those prone to inflation like food, utilities, and healthcare. Adjust your budget accordingly to ensure your spending aligns with your updated income.

- Healthcare Cost Projections: Even with a COLA, healthcare costs can be a significant drain. Factor in potential increases in Medicare premiums, deductibles, and out-of-pocket expenses when planning. The COLA helps, but dedicated healthcare savings might still be necessary.

- Investment Adjustments: If you have other investments, consider how a 3.2% COLA might affect your draw-down strategy. A higher Social Security payment might allow you to draw less from your investment portfolio, potentially extending its longevity.

- Long-Term Planning: While 3.2% is for 2026, it’s a good reminder to think about long-term inflation. Social Security COLAs are designed to help, but having diversified income streams and inflation-protected assets can further secure your financial future.

- Consult a Financial Advisor: A financial planner specializing in retirement can help you integrate COLA projections into your overall financial strategy, providing personalized advice on how to optimize your income and manage expenses.

Proactive planning, even with projected figures like the Social Security COLA 2026, empowers beneficiaries to make informed decisions and maintain financial resilience in their golden years.

Challenges and Criticisms of the COLA Calculation Method

While the COLA serves a crucial purpose, its calculation method, specifically the reliance on the CPI-W, has faced criticism. Many argue that the CPI-W, which tracks the spending habits of urban wage earners and clerical workers, does not accurately reflect the spending patterns of seniors. Retirees typically spend a larger proportion of their income on healthcare and housing, categories that often experience higher inflation rates than general consumer goods.

Critics advocate for using an alternative index, such as the Consumer Price Index for the Elderly (CPI-E), which is specifically designed to track the spending of those aged 62 and older. Studies have shown that the CPI-E often rises faster than the CPI-W, suggesting that using the CPI-W may lead to COLAs that underestimate the true cost of living increases for seniors. If the Social Security COLA 2026 were calculated using the CPI-E, it might be a higher percentage, offering more financial relief to beneficiaries.

Other challenges include:

- Lagging Indicator: The COLA is based on past inflation (third quarter data), meaning it’s a lagging indicator. Beneficiaries experience price increases throughout the year, but the adjustment only comes into effect the following January, creating a potential gap in purchasing power.

- Medicare Premium Impacts: As mentioned, rising Medicare Part B premiums can sometimes eat into the COLA, reducing the net benefit increase for some individuals.

- Political Influence: While the calculation is largely formulaic, there can be political discussions around the methodology, especially during periods of high inflation or economic strain.

These criticisms highlight the ongoing debate about ensuring Social Security benefits truly keep pace with the cost of living for its diverse recipient base. While the 3.2% projection for the Social Security COLA 2026 is a positive sign, the underlying methodology remains a point of contention for many advocates for seniors.

The Future of Social Security: Beyond the 2026 COLA

Looking beyond the immediate projection for the Social Security COLA 2026, the long-term solvency and structure of Social Security remain critical topics. While COLAs address annual inflation, they do not resolve the broader financial challenges facing the system, such as demographic shifts (an aging population with fewer workers supporting more retirees) and potential shortfalls in the trust funds.

Policymakers continually discuss various proposals to ensure the long-term health of Social Security. These may include:

- Raising the Full Retirement Age: Gradually increasing the age at which individuals can claim full Social Security benefits.

- Adjusting the Wage Base Limit: Increasing the amount of earnings subject to Social Security taxes.

- Modifying the COLA Formula: As discussed, changing the index used for COLA calculation, either to CPI-E or another measure.

- Benefit Reductions: Though highly unpopular, some proposals consider reducing benefits for future retirees or higher-income earners.

- Increased Payroll Taxes: Raising the Social Security tax rate for all workers and employers.

The Social Security COLA 2026 is an important annual adjustment, but it’s part of a larger, complex system. Understanding these broader discussions is essential for anyone concerned about the future of their retirement income. While the COLA ensures benefits keep pace with inflation year-to-year, the structural integrity of Social Security requires ongoing attention and potential legislative action to guarantee its strength for generations to come. Staying informed about both the annual COLA and these larger policy debates is crucial for current and future beneficiaries.

Maximizing Your Social Security Benefits

Beyond simply receiving the COLA, there are strategies beneficiaries can employ to maximize their Social Security benefits. While the Social Security COLA 2026 will be applied automatically, understanding how your initial benefit amount is calculated and how to optimize it can significantly impact your financial well-being throughout retirement.

- Work Longer: Each year you work beyond your initial eligibility and up to age 70 can increase your primary insurance amount (PIA). If you delay claiming benefits past your full retirement age, you earn delayed retirement credits, which provide a permanent increase to your monthly benefit. These increased benefits are then subject to future COLAs.

- Check Your Earnings Record: Regularly review your Social Security earnings record for accuracy. Mistakes can lead to lower benefits. You can access your earnings record through your my Social Security account online.

- Understand Spousal and Survivor Benefits: If you are married or widowed, you may be eligible for spousal or survivor benefits, which can sometimes be higher than your own earned benefit. Understanding these rules can help you coordinate claiming strategies with your spouse or claim the highest possible survivor benefit.

- Consider Working in Retirement: Even if you’re receiving Social Security, continuing to work can not only supplement your income but also potentially increase your future benefits if your current earnings are higher than some of your past earnings. However, be mindful of the earnings test if you claim benefits before your full retirement age.

- Education is Key: The more you understand about Social Security rules, the better equipped you’ll be to make informed decisions. The SSA website offers a wealth of resources, and financial advisors can provide tailored guidance.

By taking a proactive approach to understanding and managing your Social Security benefits, you can ensure that adjustments like the Social Security COLA 2026 contribute effectively to a secure and comfortable retirement.

Conclusion: Adapting to the 2026 Social Security COLA

The projected 3.2% Social Security COLA 2026 is a key development for millions of Americans, signaling a continued effort to protect the purchasing power of beneficiaries in an inflationary environment. While this figure is a projection and not yet official, it provides invaluable insight for financial planning. Understanding what COLA is, how it’s calculated, and its historical context allows beneficiaries to better anticipate their future income and adjust their budgets accordingly.

The economic forces driving this adjustment, alongside the ongoing debates about the COLA calculation methodology and the long-term solvency of Social Security, underscore the dynamic nature of retirement planning. For current and future retirees, staying informed, reviewing personal financial strategies, and potentially seeking expert advice are paramount. The 2026 COLA, whether it precisely matches the 3.2% projection or varies slightly, will play a significant role in the financial well-being of those who rely on these vital benefits. By adapting to these changes and planning strategically, beneficiaries can navigate the complexities of Social Security and work towards a more secure financial future.